The ZEV Mandate is Working, Industry Is On Course to Meet 2025 Targets, and Discounts are Readily Affordable - In 4 Charts

This is the fourth in a series of blogs which summarises New AutoMotive’s response to Government’s consultation on Phasing out sales of new petrol and diesel cars from 2030 and supporting the ZEV transition. You can find a summary of our consultation response elsewhere on the New AutoMotive website, as well as the earlier blogs, and the later ones when we get round to them.

Our first 3 blogs focused on the parts of Government’s consultation which considered what vehicles should be sold in the UK from 2030. Government didn’t have to consult on this, just as it didn’t consult on the original 2035 switchover date, moving it forward to 2030, or moving it back to 2035 again. No doubt, however, many will be grateful for the opportunity to air views, even if we are all ultimately looking for a swift resolution and certainty for consumers and industry.

Why, however, are we having this consultation on the potential of further support for the motor industry or regulatory flexibilities/dilutions for car makers to meet the ZEV mandate? The decision rested on 4 planks:

That many manufacturers will fall short of the ZEV mandate targets and will incur huge fines.

That estimates of organisations like New AutoMotive which show otherwise are unreliable.

That even if manufacturers have met the targets they will only have done so at unsustainable levels of discounting.

That even if manufacturers have met the targets in 2024 through a massive strain, 2025 will definitely be impossible.

How persuasive are each of those arguments? Not very.

No manufacturer will pay fines.

Our bulletin Catch-22% explains the system which allows firms to lower their targets by transferring credits for outperformance of their petrol, diesel, and hybrid/PHEV sales against easy to beat 2021 standards.

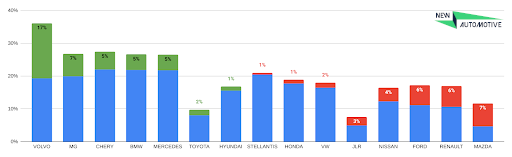

Chart 1: Over (green)/ under (red)-performance against real 2024 ZEV mandate targets (blue)

New AutoMotive’s assessment found that most manufacturers actually had real targets of 20% or less, whilst Toyota and Jaguar Land Rover’s targets were below 10%. The weighted target across the whole of the automotive industry was 18.0%

Half of the largest 16 firms who make both ICE and battery electric vehicles beat their targets. The biggest shortfall, for Mazda (who only have 1.4% share of the UK market) was 7 percentage points. And when Tesla (who only sell electric cars) and BYD (90% of whose cars are battery electric) are taken into account, 19.7% of cars sold were battery electric vehicles.

This means there is a large glut of credits - which in turn means no firm will be required to make the maximum £15K buyout payments to Government. It will be much cheaper to buy the credits from a firm which has outperformed targets and has no other use for them.

Estimates of real ZEV mandate targets are reliable.

New AutoMotive’s estimates are drawn from publicly available DVLA and DVSA data, the same sources as used by other bodies.

It’s true that we’ve had to estimate the CO₂ baselines which are used to calculate the outperformance of firms’ ICE sales, and by how much firms can thereby lower their ZEV mandate target. These have not yet been published, due to a discrepancy between UK legislation and guidance.

The DfT consultation which seeks to address this discrepancy provides a useful indicator of the level of uncertainty in CO₂ baselines.

Chart 2: Current uncertainty in industry-wide CO2 baselines

Yes, the current industry-wide uncertainty in baselines - which dictates how many CO₂ credits firms can earn in outperformance, is 0.1%. Even for a big selling firm like BMW, this translates into a movement in its real ZEV Mandate target of 0.02%. It has negligible effect on the results in chart 1.

Levels of discounting are entirely sustainable

Analysis provided to New AutoMotive by PHA AutoData, who supply Target Price data for WhatCar? and Autocar shows that the current average transaction price saving is £4,630 per car, compared to £4,336 in January 2020 (pre-pandemic levels). Based on the latest private sales figures, the current manufacturer support estimate is therefore shown below. We include the inflation-adjusted 2020 figures as a handy comparison.

Chart 3: Aggregate value of UK car discounts in 2019 and 2024, £bn (2024 prices)

The inconvenient truth is that the real-terms value of discounting today has actually fallen on pre-pandemic levels.

Manufacturers sold cars for higher margin through the pandemic and subsequent inflation and supply chain crises, but these were anomalous conditions. The re-emergence of a more normal car sales market has seen “support” offered through discounting return to normal pre-pandemic levels.

Just as 2024 targets proved to be meetable, so are those in 2025

The 2024 target wasn’t the headline 22% but - when flexibilities are taken into account - closer to 18%. The real 2025 target of 28% already looks like being close to 23%.

The good news is that industry is already meeting that target, and has been over the past 6 months, with a battery electric market share of 23.4%.

Chart 4: Over (green)/ under (red)-performance against real 2025 ZEV mandate targets (blue) over the past 6 months

Four of the largest 10 car manufacturers - including VW Group, which sold more EVs than second place Stellantis and third placed Hyundai put together - are in credit. When Tesla and BYD are taken into account, we are again on course for an excess of credits.

It’s them, not us

So what is all the fuss about?

In essence, this has nothing to do with the ZEV mandate. The UK hosts some lagging manufacturers.

For any of these firms to claim the demand isn’t there for EVs is a nonsense.

One half of Jaguar Land Rover has never yet produced an EV. The other half has elected to stop selling any cars in 2025. Toyota, the biggest selling car maker in the world, produces just one EV model.

Finally Nissan, which offers only 2 EVs, one very dated and the other which is overpriced and unpopular, is having a global crisis that has nothing to do with the ZEV mandate. What Nissan really needs is not protection from the ZEV mandate but from a competitive global market. Given that the UK Government can’t help with that, its best bet is to fund a bailout, support a restructure, or help with finding a buyer for the Sunderland site.

The worst thing it can do is to shaft the manufacturers who have been investing in good faith, the charge point and infrastructure providers and our future clean air commitments by weakening the ZEV mandate.